Stablecoins: Crypto’s Killer Use Case

Money is constantly evolving. While cash and online bank accounts remain the primary tools for transactions today, this won’t be the case for long. A new form of digital money has emerged, one that moves faster, works globally, and operates without the inefficiencies of the legacy financial system.

Enter stablecoins: a unique form of cryptocurrency that moves trillions of dollars each month and now facilitates more daily transaction volume than Visa and Mastercard combined. Most people still think of cryptocurrency as volatile, speculative, and risky. But not all crypto assets are designed this way. That’s why leading institutions like PayPal, Bank of America, and JPMorgan are building and scaling new stablecoin solutions.

This article aims to fully unpack what stablecoins are, what the different types are, and where this exciting new asset class is headed next.

What are Stablecoins?

Stablecoins are a class of cryptocurrency designed to maintain a stable value, typically pegged to a traditional asset like the U.S. dollar, gold, or other financial benchmarks. Unlike most other cryptocurrencies such as Bitcoin or Ethereum, stablecoins offer predictability and reliability, making them essential to the growing digital economy.

The extent of adoption is evident in the numbers. By the end of 2024, stablecoins were involved in over two thirds of all onchain transactions, and the total stablecoin supply across all major projects now exceeds $230B.

Beyond serving as a liquidity source in crypto-native markets, stablecoins also act as act as a global dollar liquidity pool, enabling:

- Efficient trading and settlements: Traders and investors use stablecoins as a safe intermediary when moving between assets.

- Borderless payments: Stablecoins allow users to send and receive money globally, often with lower fees and faster settlement times than traditional banking rails.

- Protection against inflation: In emerging markets and unstable economies, stablecoins provide a dollar-pegged alternative to weak local currencies.

However, not all stablecoins function the same way. They differ in their mechanisms for maintaining stability, collateralization methods, and degree of decentralization.

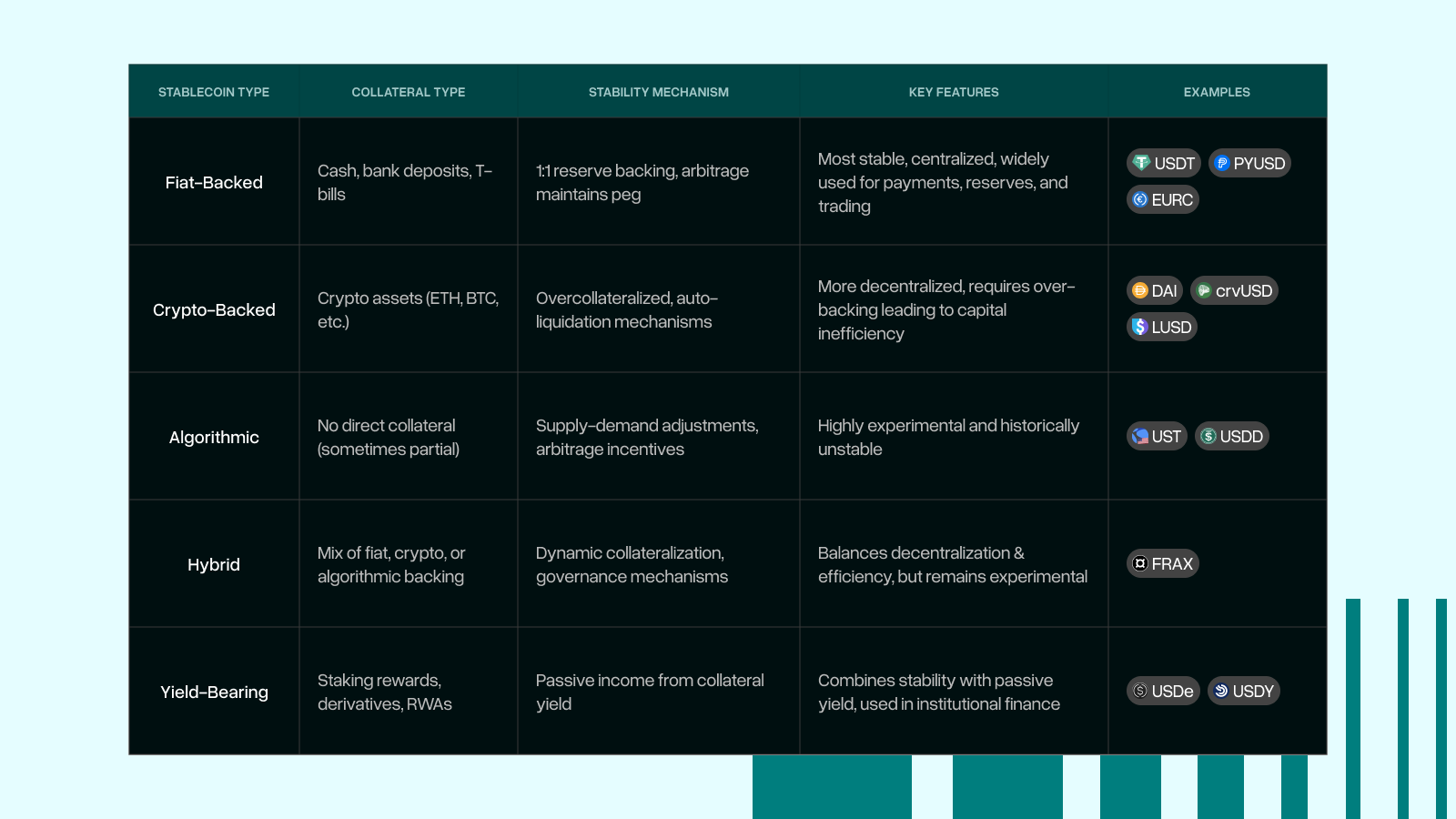

The Five Main Categories of Stablecoins

Stablecoins share the goal of maintaining a stable value, but the methods vary widely. Some rely on traditional financial reserves, while others use crypto collateral, algorithmic mechanisms, or yield-generating assets. These structural differences affect everything from stability and capital efficiency to regulatory scrutiny and adoption.

Fiat-Backed Stablecoins

Fiat-backed stablecoins are the most common type and are designed to maintain a 1:1 peg with traditional currencies, such as the U.S. dollar or euro. They achieve this peg through direct fiat reserves and market arbitrage. If the price falls below $1, traders buy the stablecoin at a discount and redeem it for $1 in cash through whitelisted entities. This reduces the token supply and restores the peg.

If the price rises above $1, traders mint new stablecoins with $1 of fiat and sell them at a premium, increasing supply and rebalancing the price. This continuous backing by fiat assets ensures reliability and scalability.

These stablecoins are issued by companies that maintain reserves in banks, cash equivalents, Treasury bills, or government securities. For example, Tether’s USD₮, the world's largest stablecoin, is backed by a mix of cash, U.S. Treasury bills, and other secure, liquid assets. This ensures redemption demands can be met at all times.

Fiat-backed stablecoins are considered the most stable and widely adopted. They are integrated across crypto exchanges, DeFi applications, and payment networks. However, they require trust in the issuer and have drawn regulatory scrutiny, prompting companies like Tether to regularly publish reserve attestations.

Crypto-Backed Stablecoins

Crypto-backed stablecoins use cryptocurrency as collateral instead of fiat. Due to volatility, these must be over-collateralized. For every $1 issued, more than $1 worth of crypto is locked up to ensure backing even during price drops.

The most well-known example is DAI, issued by MakerDAO. Users deposit collateral (like ETH or wBTC) into a Maker Vault. To generate $1,000 of DAI, one might need to lock up $1,500 of ETH. If collateral falls too much in value, the system automatically liquidates some to maintain solvency.

These stablecoins are more decentralized and transparent, with verifiable onchain reserves. But their reliance on volatile assets makes them less capital-efficient, and sharp market downturns can trigger cascading liquidations.

While successful, crypto-backed stablecoins like DAI often depend partly on centralized stablecoins (like USDC), raising questions about their true decentralization and scalability.

Algorithmic Stablecoins

Algorithmic stablecoins attempt to maintain their peg through automated supply and demand mechanisms, without collateral. They use economic incentives to keep prices stable.

A common design involves a dual-token system. One token acts as the stablecoin; the other absorbs volatility. TerraUSD (UST) was the most well-known example. When UST dropped below $1, it could be burned in exchange for LUNA, reducing supply. If UST exceeded $1, LUNA could be burned to mint new UST.

This system worked until it didn’t. When UST lost its peg, confidence in LUNA collapsed, triggering mass sell-offs and hyperinflation. LUNA and UST had market caps of ~$40B and ~$18B respectively before crashing, marking one of crypto’s most dramatic failures.

Other algorithmic models, like rebase tokens or coupon-based systems, have also struggled. Since Terra’s collapse, purely algorithmic models have fallen out of favor in favor of hybrid or collateralized approaches.

Hybrid Stablecoins

Hybrid stablecoins combine features of collateralized and algorithmic models. Using partial reserves and algorithmic stabilization, they aim for capital efficiency and resilience.

These often employ fractional collateralization, only part of the supply is backed by real assets. The rest relies on a mechanism (like a secondary token) to maintain the peg.

Frax (FRAX) is a prominent example. It launched as a fractional-algorithmic stablecoin, backed partly by collateral and partly by an algorithm. However, Frax has since transitioned to full collateralization to improve stability.

While theoretically sound, hybrid stablecoins rely heavily on market confidence. If trust in their mechanism or secondary token weakens, the peg can break. This makes them less proven at scale compared to fiat- or crypto-backed options.

Yield-Bearing Stablecoins

Yield-bearing stablecoins offer stability and passive income by distributing earnings from staking, arbitrage, or tokenized real-world assets. Two notable examples are Ethena’s USDe and Ondo’s USDY.

Ethena’s USDe is collateralized by staked assets like ETH. It uses a delta-neutral strategy, combining ETH staking with short positions in derivative markets. This neutralizes price exposure while generating yield, creating a synthetic dollar without direct fiat backing.

Ondo’s USDY, by contrast, is backed by U.S. Treasuries and distributes daily yield based on those returns.

These stablecoins are appealing for passive income, but carry new risks: derivative exposure, counterparty issues, and regulatory uncertainty regarding tokenized securities.

Which Stablecoin is the Best?

There’s no universal answer. But as of 2025, Tether’s USD₮ remains the most dominant and widely used:

- Market dominance: $150B+ market cap (~65% of dollar-backed supply)

- Liquidity: Most used trading pair across exchanges

- Resilience: Has weathered multiple crises, including USDC’s temporary depeg in 2023

- Multi-chain presence: Available on Ethereum, Tron, Solana, Polygon, BSC, and more

- Global usage: Especially in emerging markets, for remittances and savings

Still, the “best” stablecoin is evolving. What matters more is where the category is headed.

The Future of Stablecoins

Stablecoins today operate on blockchains not optimized for them. High fees, congestion, and slow finality hold back adoption.

That’s why Plasma exists—a purpose-built blockchain for stablecoin payments. It combines gasless USD₮ transactions and Bitcoin-grade security to provide a more efficient foundation for stablecoins.

In the long run, the winners in stablecoins will be those with both strong market trust and the right infrastructure, optimized for speed, security, and scalability. Stablecoins aren’t just a crypto use case. They’re a new base layer for global finance.

Disclaimer

This announcement is for informational purposes only and is not, and is not intended to be, an offer or sale of securities or the XPL tokens. Any offer or sale of the XPL Tokens will only be done subject to the applicable terms and conditions, which will be available upon the opening of the deposit period, and pursuant to definitive offering documents, which will be available upon the closing of the deposit period for those participants who have proven their eligibility via Sonar by Echo. Sonar provides infrastructure services to Plasma only and does not conduct any offer or sale of the XPL Tokens.

We do not consider the offer or sale of the XPL tokens to be securities transactions but due to the lack of clarity of applicability of the securities laws in the United States and foreign jurisdictions, only those participants who have proven their eligibility via Sonar by Echo will be considered as eligible participants. XPL Tokens have not been registered under the U.S. Securities Act of 1933 or any state securities laws and are being offered in reliance on exemptions from registration. As such, they are subject to restrictions on transferability and resale and may not be transferred or resold except as permitted under applicable laws.

The Plasma website and the information contained herein are for informational purposes only. Information contained herein contains “forward-looking statements” that express or involve discussions with respect to predictions, expectations, beliefs, plans, projections, objectives, goals, assumptions, or future events or performance and are not statements of historical facts. Forward-looking statements are based on expectations, estimates and projections at the time the statements are made and involve a number of risks and uncertainties which could cause actual results or events to differ materially from those presently anticipated. Neither Chain Technologies Research nor Plasma Foundation can provide any guarantee or certainty with respect to any forward-looking statement.

.png)

.png)